Understanding How Usage Credits Affect Your Monthly Electricity Bill Can Help You Decide if These Plans Will Save You Money or Cost You More

Key Takeaways

- Bill credit plans offer a specific dollar discount on your energy bill when you use a targeted amount of electricity each month.

- Hitting the exact usage tier is critical, as falling into the “donut hole” of missing the required kilowatt-hours (kWh) results in a massive price spike.

- Evaluating your energy consumption history is the best way to uncover the true math behind advertised teaser rates and decide if the plan fits your home’s energy habits.

A bill credit plan offers a flat monetary discount on your average monthly electric bill when you consume a specific amount of power, but it comes with hidden financial risks that can trap unsuspecting consumers. While scoring a massive $100 discount sounds like a brilliant way to save money in a deregulated energy market, falling just one kilowatt-hour short of the required usage tier plunges you into a costly “donut hole,” completely wiping out your savings and leaving you with an inflated base rate. By diving into the fine print of these contracts and evaluating your energy consumption history, you can avoid costly teaser rates and determine if these tiered electricity plans are actually a smart financial move for your household.

Bill Credit Usage Calculator

What Is a Bill Credit Electricity Plan?

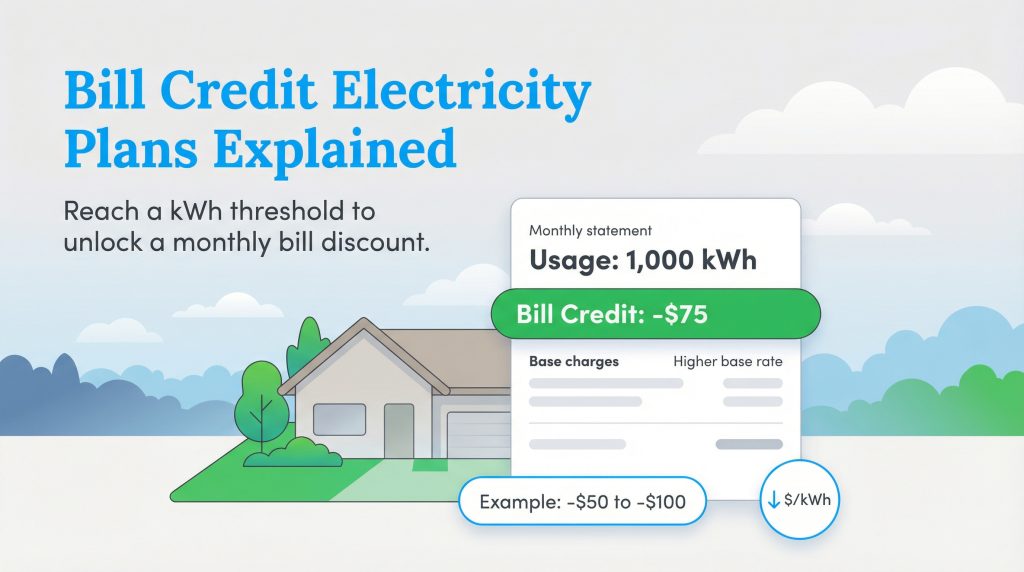

When comparing your electric plan options, you will inevitably notice offers promising a significant financial discount if you reach a certain threshold. A bill credit electricity plan provides a flat monetary discount — typically anywhere from $50 to $100 — directly applied to your average monthly electric bill. However, you only unlock this generous reward by crossing a very specific kilowatt-hour limit during a standard 30-day billing cycle. Most retail energy providers structure these aggressive incentives around standard benchmark tiers like 500, 1,000, and 2,000 kWh.

Understanding how these plans operate in daily practice requires looking past the bold numbers on a marketing brochure. Think of a bill credit electricity plan as a high-stakes incentive program. The underlying base rate for the electricity itself is typically much higher than standard market prices. The moment your home consumes enough energy to cross that specific threshold, the provider automatically applies the credit to your account. This sudden discount offsets the higher base cost of the power, artificially dropping your effective rate per kWh for that particular billing cycle.

How kWh Usage Credits Work

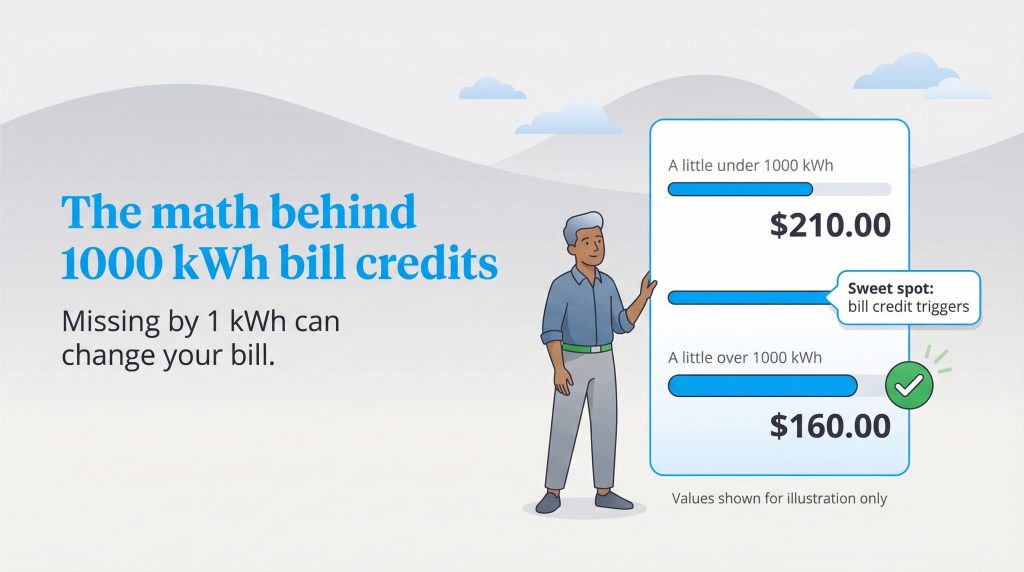

Providers heavily market the 1,000 kWh bill credit plan because 1,000 kWh is the most commonly used benchmark in advertised average-price tables across shopping portals. They broadcast an incredibly low price, but that number only exists as a reality if the discount perfectly applies. The underlying base rate might actually sit closer to 16 cents per kWh, creating a massive discrepancy if you miss the target.

Missing the target by a single kilowatt-hour dramatically shifts your financial reality. To avoid falling into this trap, you need to see exactly how the numbers play out across different property sizes. Below is a simplified breakdown showing why hitting the exact sweet spot matters, demonstrating the harsh reality of the effective rate per kWh.

| Usage Level | 500 kWh (Small Apartment) | 1,000 kWh (Medium Home) | 1,500 kWh (Large Home) |

|---|---|---|---|

| Base Rate Cost | $80 Base Cost | $160 Base Cost | $240 Base Cost |

| Discount Status | No Credit Applied | $61 Credit Applied | No Credit Applied |

| Resulting Bill | $80 Total Bill | $99 Total Bill | $240 Total Bill |

| Effective Rate per kWh | 16¢ per kWh | 9.9¢ per kWh | 16¢ per kWh |

Pros and Cons of a Tiered Electricity Plan

Every energy contract involves trade-offs. Before locking into long-term tiered electricity plans that hinge on your ability to consistently manage your power volume, carefully weigh the benefits against the potential drawbacks. It pays to understand the reality of fluctuating seasonal consumption before making a commitment.

Pros

- High maximum savings: You can achieve some of the lowest effective rates on the market if your home perfectly hits the usage window.

- Rewards consistent usage: Excellent for households that carefully track their historical usage and maintain highly predictable energy habits year-round.

- Offset higher summer bills: A well-placed credit can help soften the financial blow when your air conditioning runs non-stop during the hottest months.

Cons

- The cliff effect: Missing your target by a tiny margin results in a massive price spike due to an inflated underlying energy rate.

- Seasonal fluctuation risk: Mild weather months (like October or April) naturally cause your consumption to drop, risking the loss of your discount.

- Rigid requirements: Failing to actively track your meter readings can turn a seemingly cheap plan into an incredibly expensive mistake.

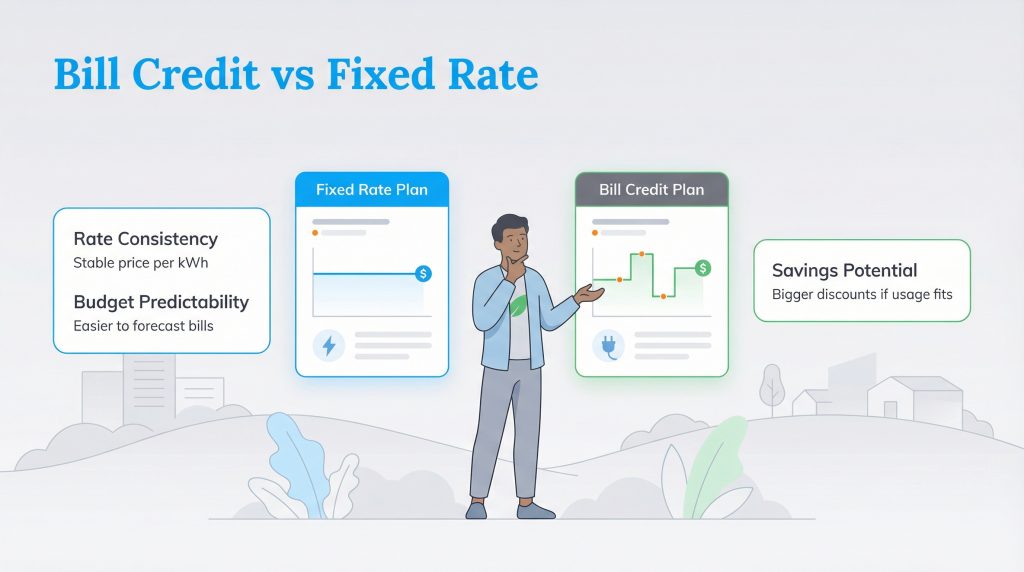

Fixed Rate vs Bill Credit: Which Is Cheaper?

When evaluating a fixed rate vs bill credit plan, the biggest difference ultimately comes down to your personal risk tolerance and living situation. A true fixed-rate plan charges the exact same price per kilowatt-hour regardless of how much energy your household consumes. Conversely, credit-based options offer potentially steeper discounts but carry significant volume risk. If your habits fluctuate, you miss the discount window entirely.

Retail energy providers like Gexa Energy frequently offer these credit-based structures to attract shoppers looking for the absolute lowest advertised price on platforms like the Texas official Power to Choose marketplace. To ensure you lock in the best rate for your specific needs, follow these hard-and-fast rules when selecting your next contract:

- Choose a fixed-rate plan if you live in an apartment. Small living spaces rarely use enough energy to clear a 1,000 kWh tier, making standard fixed rates the cheapest and safest option.

- Choose a fixed-rate plan if your usage fluctuates. If you travel frequently or have highly variable seasonal usage, securing a stable price per kWh protects you from sudden bill spikes during mild weather months.

- Choose a bill credit plan if you have a large home with consistent usage. If you run a pool pump year-round, charge an electric vehicle daily, or possess a massive multi-zone HVAC system, you will easily hit the threshold and secure massive discounts.

The Texas Teaser Rate Danger Zone

In a deregulated energy market, retail providers purchase power on the wholesale market and resell it to residential customers. To keep their own costs stable, these companies require customers with highly predictable usage patterns. To attract these ideal consumers, retail providers frequently deploy a marketing tactic known as the Texas teaser rate. This refers to an artificially low advertised price that assumes your household will perfectly hit the exact usage tier required to trigger their massive discount.

Because the average consumer usually just glances at the bolded price on a marketing flyer, they often miss the underlying base rate entirely. The math changes drastically the moment you use a little more or a little less power, placing your budget directly into the danger zone. Here is exactly what happens if you fall into the “donut hole” by hitting 999 kWh instead of 1,000 kWh:

- The promotional credit vanishes. The promised statement credit is immediately voided for the entire billing cycle.

- Your base rate inflates. Instead of paying the advertised 9.9 cents per kWh, you revert back to the hidden underlying rate, which often exceeds 16 cents per kWh.

- You pay more for using less. Because the massive discount disappears, a monthly statement for 999 kWh can easily cost $40 to $60 more than a statement for 1,001 kWh.

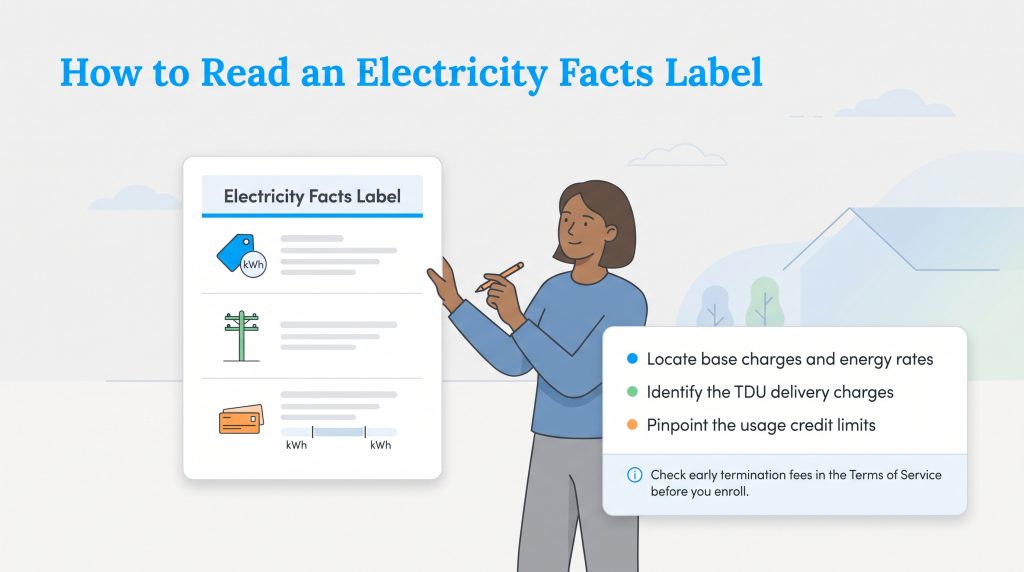

How to Read the Electricity Facts Label

The Electricity Facts Label (EFL) acts as the ultimate nutrition label for energy plans. It strips away flashy marketing jargon and exposes the true cost of the product you are about to purchase. Learning how to properly review this legally required document addresses the most critical step you can take to protect your wallet from deceptive pricing.

Before you agree to any new contract or provide your service address, pull up this standardized sheet and verify the math. Use this simple three-step checklist to find exactly where the true costs hide:

- Locate the base charges and energy rates. Look past the top average price chart to find the distinct “Energy Charge” line item. This tells you exactly what you pay per kWh if you miss the discount window.

- Identify the TDU delivery charges. Find the specific line detailing the TDU delivery charges. These are regulated utility fees passed directly to you for maintaining local poles and wires, and they still apply even if a usage credit offsets your energy charge.

- Pinpoint the specific credit threshold limits. Look for the “Usage Credit” section directly underneath the base charges. Note the exact minimum and maximum kWh limits required to successfully trigger the discount.

Evaluating Your Energy Consumption History

Purposefully leaving lights on or running appliances just to hit a 1,000 kWh threshold defeats the entire purpose of conservation. Wasting power to secure a discount isn’t an environmentally mindful choice. Instead, you should focus on proven strategies to save on your electric bill through natural efficiency and select a plan that naturally fits your existing consumption profile.

Deciding whether these aggressive pricing structures fit your lifestyle requires a ruthlessly honest assessment of your historical data. Deregulated market choices extend well beyond just one or two states. Whether you live in the South or are comparing options on PA Power Switch, you must understand your usage volume before signing up. Take these exact actionable steps to evaluate your energy consumption history today:

- Log into your current provider portal. Access your online account through your existing electric company or your local utility’s smart meter dashboard.

- Pull the past 12 months of usage data. Navigate to the billing or usage tab and download your kilowatt-hour totals for a full calendar year to capture both summer peaks and mild winter lows.

- Pinpoint your lowest usage month. Identify the single month where you consumed the least amount of electricity. If this lowest number still clears the 1,000 kWh benchmark, you are a prime candidate for a usage credit. If it falls below the mark, a fixed-rate plan is a much safer bet.

Making Your Final Electricity Plan Choice

Harnessing a targeted discount can serve as a fantastic financial tool, provided you understand your historical energy usage perfectly. These tiered programs deeply reward consistency, but they demand your active participation to ensure a high base rate doesn’t catch you off guard during a mild month. Take control of your data, read the fine print on the EFL, and maintain a clear view of your monthly meter readings.

Ultimately, selecting the right energy contract is about matching the product to your lifestyle. If you own a large property with high, steady energy demands, chasing those massive bill credits can substantially lower your average monthly electric bill. However, if you live in a smaller space or travel frequently, prioritizing the unshakeable stability of a standard fixed rate provides far better long-term peace of mind. Review your numbers carefully, bypass the deceptive marketing tactics, and choose an energy plan that truly supports your household’s daily rhythms.

Frequently Asked Questions About Bill Credit Electricity Plans

Are bill credit plans considered fixed-rate plans?

What is a Texas teaser rate?

Which energy providers offer the best bill credit electricity plans?

Do bill credit plans roll over to the next month?

What happens if I use less electricity than my bill credit tier requires?

What happens if I use 999 kWh on a 1,000 kWh bill credit plan?

Do bill credit plans include TDU delivery charges in the advertised rate?

Are bill credit plans only available in Texas?

Why do electric companies offer usage credits?

Can I get a bill credit plan with renewable energy?

How do I know my average monthly electricity usage?

About the Author

LaLeesha has a Masters degree in English and enjoys writing whenever she has the chance. She is passionate about gardening, reducing her carbon footprint, and protecting the environment. She also recently served as President of the Board for City Sprouts (a community garden).

David has been an integral part of some of the biggest utility sites on the internet, including InMyArea.com, HighSpeedInternet.com, BroadbandNow.com, and U.S. News. He brings over 15 years of experience writing about, compiling and analyzing utility data.