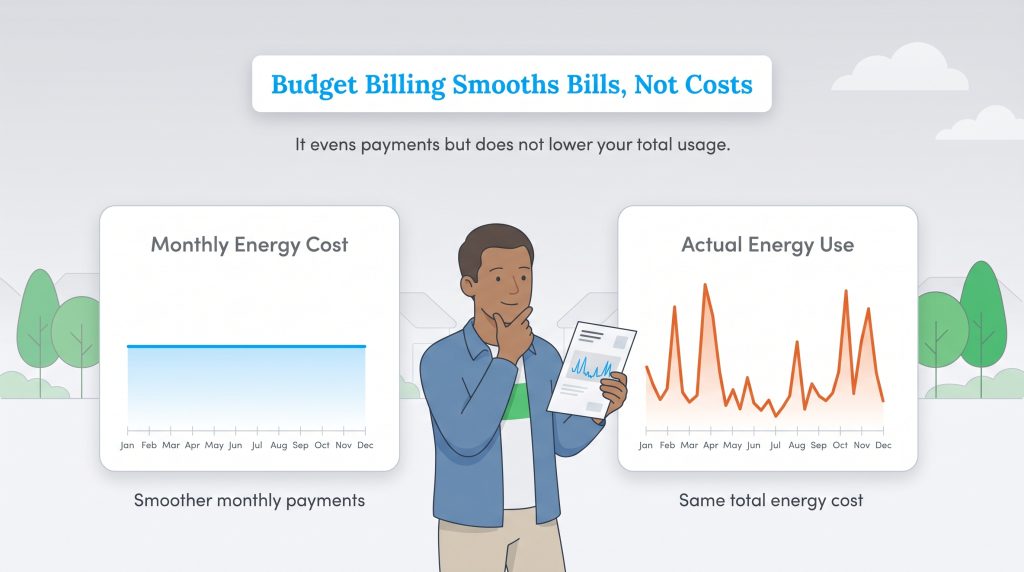

Budget billing smooths out your utility payments to avoid seasonal spikes, but it doesn’t lower your total energy costs.

Key Takeaways

- Budget billing averages your annual energy usage into predictable monthly payments.

- You may still owe a “true-up” balance at the end of the year if you use more energy than estimated.

- Monitoring your actual usage is a smart way to ensure the plan works for your financial goals.

Opening your utility bill during a heatwave or a cold snap can feel like a gamble, with prices often jumping hundreds of dollars higher than you expected. At UtilitiesForMyHome.com, we know that if you live on a fixed income or simply prefer knowing exactly how much money leaves your bank account each month, utility provider payment plans offer a highly effective solution to that financial roller coaster. While it won’t lower the total amount you pay for energy over the entire year, enrolling in an average payment plan transforms volatile seasonal bills into a steady, fixed monthly payment that makes planning your household budget significantly easier and virtually stress-free.

What Is Budget Billing?

What is budget billing? It is an average payment plan that smooths out seasonal spikes by calculating your annual electricity or natural gas consumption and dividing it into 12 equal monthly installments. This ensures your fixed utility payments stay the exact same price every month, helping you avoid seasonal utility spikes during extreme winter or summer weather.

Budget billing is a popular program offered by most electric and natural gas providers across the country. Instead of paying for exactly what you consume on a month-to-month basis — which inevitably results in high bills in the summer and winter and low bills in the spring and fall — you pay a predictable rate. It is important to understand that this is strictly a payment strategy designed for consumer convenience. It is not a discount program, and it does not reduce the base rate you pay for your energy supply or delivery.

Depending on your specific utility provider, you might see this program listed under several different names on their website. Common variations include “Level Payment Plan,” “Average Monthly Billing,” or “Balanced Billing.” In simple terms, you trade off seeing your exact monthly costs on your statement for smoother, more consistent payments. Just remember, securing predictable payments doesn’t replace the need to monitor your own home usage if you genuinely want to keep both your deferred balance utility bill and your carbon footprint in check.

How Utility Companies Calculate Your Budget Billing Amount

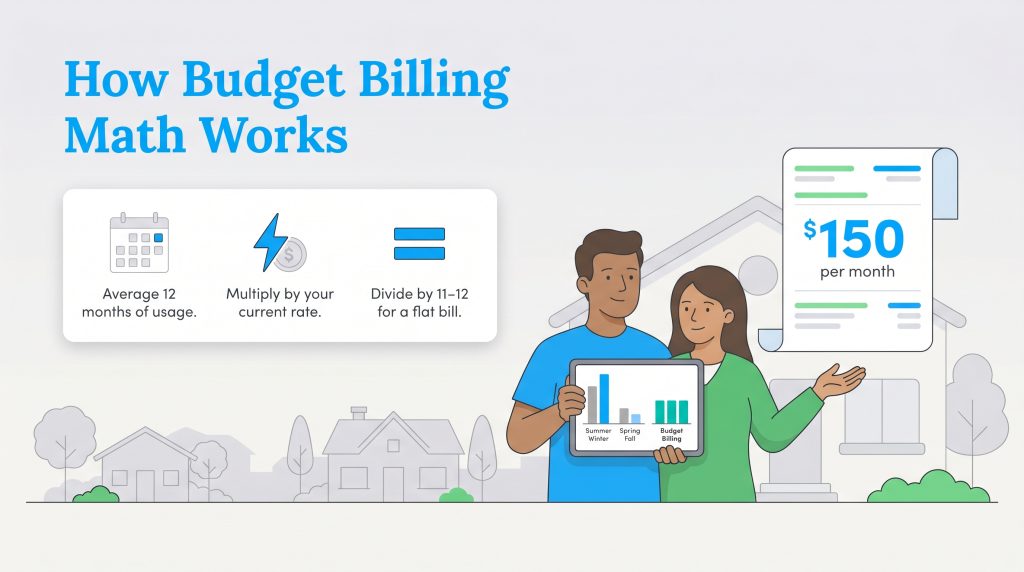

Utility companies use a relatively straightforward mathematical method to determine your new monthly payment amount. Their primary goal is to ensure that by the end of your 12-month budget billing reconciliation cycle, you have paid for exactly the amount of energy you consumed, just delivered in equal installments. Here is the step-by-step math most providers use to establish your rate:

- Average the last 12 months of usage: The utility provider looks at the total energy consumption history for your specific address over the previous year. If you are new to the home, they may estimate this baseline using data from similar properties in your neighborhood.

- Apply the current rate: They multiply that historical usage by the current market rate for electricity or natural gas. They often factor in expected inflation or upcoming state energy price hikes to ensure the estimate is as accurate as possible.

- Divide by 11 or 12: Finally, they take that total estimated annual cost and divide it by 11 or 12 months to create your fixed monthly payment. The division depends on whether your provider utilizes a dedicated 12th month solely for account reconciliation.

To visualize how this math works in the real world, let’s assume your household consumes an average of 12,000 kilowatt-hours (kWh) of electricity per year. If your local utility company charges an average rate of 15 cents per kWh, your total annual electricity cost is $1,800. Under standard billing, you might pay a massive $300 bill during a scorching July and a tiny $75 bill in a mild April. However, with an average payment plan, your provider simply takes that $1,800 annual total and divides it by 12 months. Your resulting fixed payment is securely set at $150 per month, every month, regardless of the season.

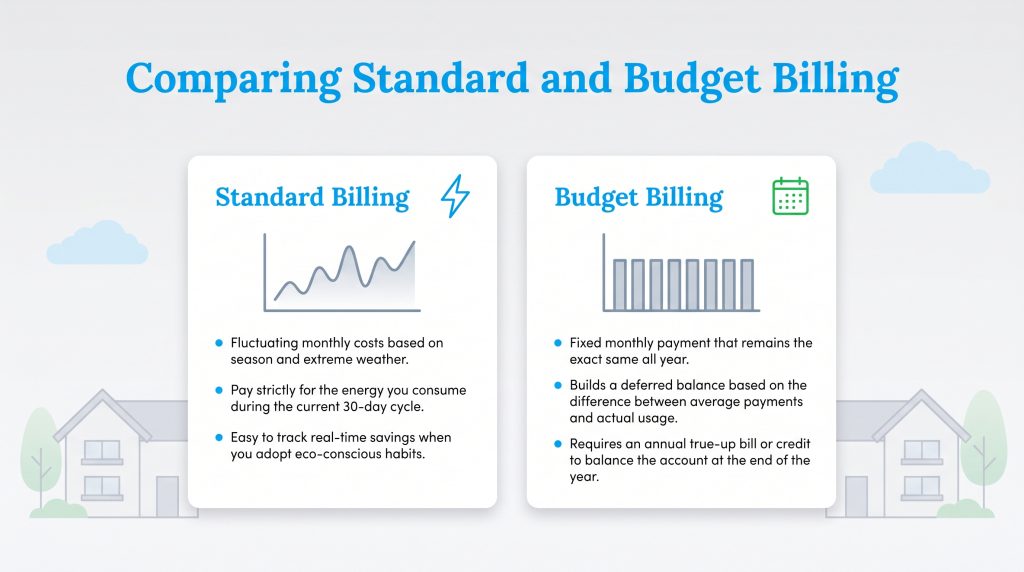

Comparing Standard Billing And Budget Billing

Understanding the exact differences between a standard payment structure and an average payment plan is the best way to determine which option suits your household. Standard billing focuses strictly on your real-time usage, while budget billing emphasizes long-term financial stability. Here is a direct comparison of the two models.

| Standard Billing | Budget Billing |

|---|---|

| Fluctuating monthly costs based on season and extreme weather. | Fixed monthly payment that remains the exact same all year. |

| Pay strictly for the energy you consume during the current 30-day cycle. | Builds a deferred balance based on the difference between average payments and actual usage. |

| Easy to track real-time savings when you adopt eco-conscious habits. | Savings from eco-conscious habits take months to reflect in your lowered payment amount. |

| No annual reconciliation or settlement month required. | Requires an annual true-up bill or credit to balance the account at the end of the year. |

Understanding The True-Up Bill And Reconciliation

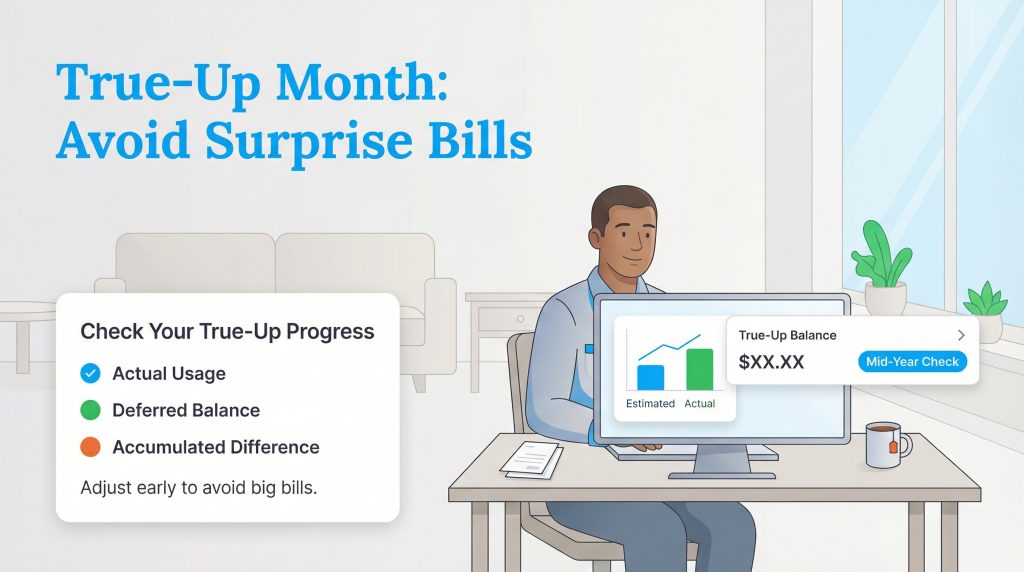

The most notoriously confusing aspect of budget billing for many customers is the budget billing reconciliation period. Because your monthly payments are based on a historical estimate, they rarely match your actual usage perfectly down to the penny. Eventually, the utility company has to balance their books during what is known as the settlement month.

Throughout the year, your utility provider tracks your deferred balance — the running tally of the difference between the fixed amount you have paid so far and the actual cost of the energy you have consumed. During the 12th month of your billing cycle, the provider compares these two numbers to close out the year.

If you underpaid because you used more energy than the company estimated, you will owe a true-up bill. This means the negative deferred balance becomes due as a single lump sum. This bill shock often catches customers off guard after an unusually harsh winter or scorching summer. Conversely, if you overpaid because you used less energy than predicted, the utility will credit your account for the overpayment or issue a refund check.

To avoid a massive true-up bill, you should prioritize understanding your electric bill by checking your digital or paper statement every single month. If you spot a growing negative deferred balance by mid-year, you can proactively call your provider to slightly increase your monthly payment amount. Better yet, review our guide on how to save on your electric bill to implement practical, energy-saving home habits that actively bring your usage down before your settlement month arrives.

Pros And Cons Of Budget Billing

Deciding whether to enroll in budget billing is largely a matter of financial preference and personal organization. It works beautifully to reduce financial anxiety for some households, but it heavily frustrates others. Reviewing the pros and cons of budget billing can help you determine if this utility strategy aligns with your goals.

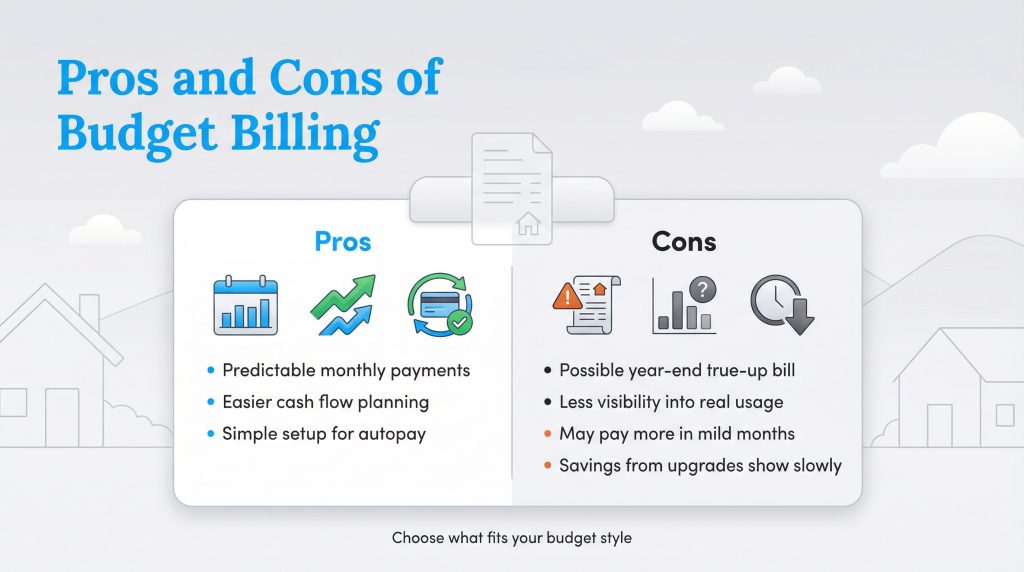

- Pros of Budget Billing:

- Predictable Budgeting: Enjoy fixed monthly payments that make household financial planning effortless.

- Avoid Seasonal Spikes: Protect your wallet from massive, unexpected utility bills during extreme winter and summer weather.

- Easier for Shared Housing: Splitting a flat, predictable bill is significantly simpler for roommates sharing expenses.

- Cons of Budget Billing:

- True-Up Bill Shock: High risk of facing a massive settlement balance at the end of the year if your usage was underestimated.

- Lack of Conservation Incentive: Because your bill doesn’t change immediately, you lose the psychological push to turn off lights and conserve energy.

- Delayed Return on Investment: If you add solar panels or upgrade to an efficient HVAC system, it takes months for your average monthly billing amount to drop.

Does Budget Billing Actually Save You Money?

Budget billing does not reduce the total cost of utilities; it only evens out your cash flow so you aren’t hit with massive spikes. In other words, you do not actually save any money by enrolling in an average payment plan. You are simply rearranging when and how you pay the utility provider for the power you already used.

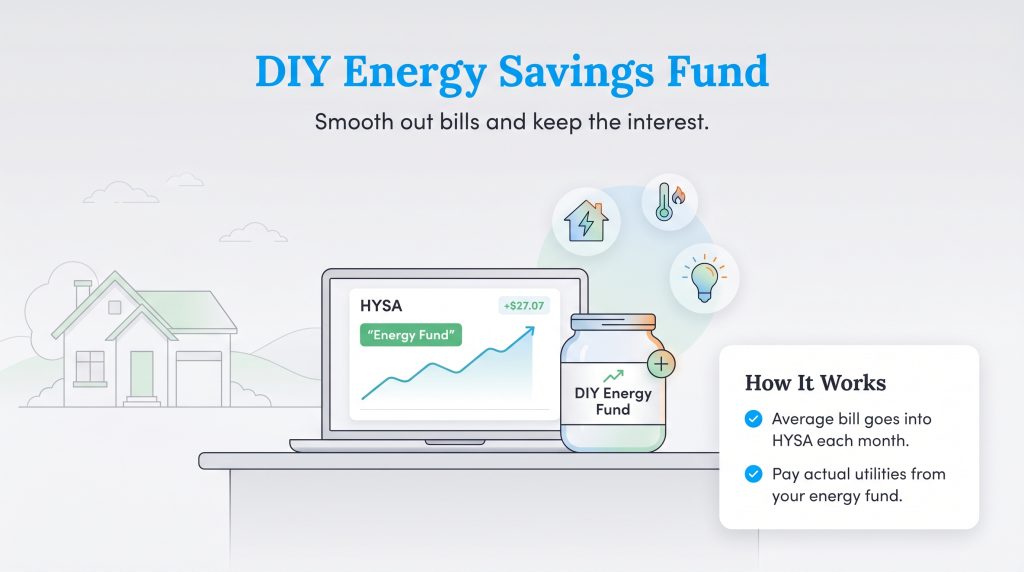

Creating A DIY Energy Savings Fund

If you genuinely want a predictable bill but dislike the idea of the utility company holding onto your overpayments during mild months, there is a smart financial alternative: act as your own utility provider and create a DIY energy savings fund. Calculate your average monthly cost and transfer that exact amount into a High-Yield Savings Account (HYSA) every single month. When your fluctuating utility bill arrives, pay the actual cost directly from this dedicated fund.

During low-usage spring and fall months, the fund will grow. During high-usage summer and winter months, you will have enough cash saved up to seamlessly cover the spike. The major benefit here is that you earn the interest on the extra cash sitting in the account, not the utility provider. To do this effectively, research how to estimate appliance energy use to set a realistic monthly contribution goal for your personal fund.

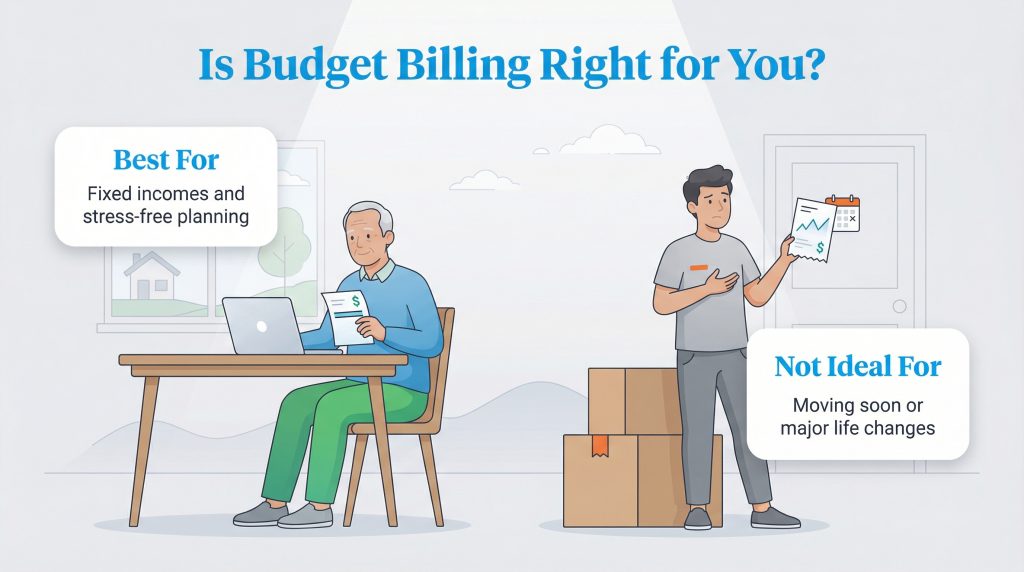

Deciding If An Average Payment Plan Is Right For You

Budget billing is an excellent tool for specific types of residents but can easily become a major hassle for others. The ideal candidates for an average payment plan are strict budgeters, retirees living on a fixed income, and homeowners located in extreme climates prone to massive seasonal temperature swings. If you plan on staying in your current home for several years and rarely make major changes to your energy habits, the stress-free convenience of a fixed monthly payment far outweighs the risks of the settlement month.

On the other hand, you are a poor candidate for budget billing if you plan to move within the next 12 months, as closing your account forces an immediate true-up bill that can ruin your moving budget. It is also an ill-advised strategy if you are expecting major life changes (like welcoming a new baby) or actively adding high-draw appliances like an electric vehicle (EV) charger to your garage. If you are an intensive budgeter who wants to see real-time financial rewards for taking shorter showers and turning off the lights, the delayed nature of budget billing will likely leave you deeply frustrated.

Before you commit to a utility provider payment plan, log into your online portal and review your last 12 months of billing statements. Decide if those seasonal spikes cause you genuine financial anxiety. If finding an extra $150 to cover the air conditioning in July causes stress, pick up the phone, contact your utility company, and ask for an estimated budget billing quote today.

Frequently Asked Questions About Budget Billing

Does budget billing save you money?

No, budget billing does not lower your utility rates or total annual cost. It simply spreads your payments out evenly over the year. To save money, you must reduce your overall energy consumption by implementing efficiency upgrades or shifting your usage to off-peak hours.

What happens to my budget billing if I move?

When you move and close your utility account, you are immediately removed from the budget billing program. This triggers an instant reconciliation process. If you have a negative deferred balance, you will owe the entire amount on your final bill. If you overpaid, the provider will cut you a refund check.

Do I have to pay a true-up bill if I cancel budget billing early?

Yes. If you voluntarily unenroll from the program before your 12-month settlement month arrives, the utility company must settle your account. Any unpaid deferred balance for the energy you already used becomes due immediately on your next standard statement.

Can my utility provider change my budget billing amount mid-year?

Yes, and they frequently do. Utility providers usually review your account quarterly. If your actual usage drastically outpaces their initial estimates — or if regional energy rates suddenly spike — they will proactively increase your fixed monthly payment to prevent you from drowning in a massive true-up bill at the end of the year.

Can I get money back from budget billing?

Yes. If you used less energy than the utility estimated by the end of your settlement period, you will typically receive a bill credit that rolls over and applies to your next billing cycle. Some providers may issue a physical check or direct deposit if the overpaid credit is significant.

Is average monthly billing the same as budget billing?

Yes, in most cases. Most utility companies use these specific terms interchangeably across their platforms. Whether it is called level pay, balanced billing, or average monthly billing, the underlying concept of averaging your annual utility costs into equal monthly payments remains exactly the same.

Can budget billing hurt my credit score?

Generally, no. Enrolling in the program itself does not require a hard credit pull, nor does it inherently affect your credit score. However, just like standard billing, if you fail to make your required payments on time or leave a large unpaid true-up balance after closing your account, that delinquency will eventually be reported to major credit bureaus.

Can I sign up for budget billing if I just moved into a new home?

Yes, though it depends on your specific utility provider’s rules. If they allow it, the company will typically base your estimated monthly payments on the historical energy usage of the previous tenants. If the home is brand-new construction and lacks a usage history, they may estimate your payment based on the square footage of the property and typical neighborhood consumption.

What happens if I miss a budget billing payment?

Missing a payment is particularly risky when enrolled in a level payment plan. Most utility companies have strict policies that will automatically remove you from the program if you miss a single payment or pay late. If removed, any deferred balance you owe immediately becomes due on your next billing cycle alongside late fees.

About the Author

LaLeesha has a Masters degree in English and enjoys writing whenever she has the chance. She is passionate about gardening, reducing her carbon footprint, and protecting the environment. She also recently served as President of the Board for City Sprouts (a community garden).